Contributed by: TD Insurance, an Engineers Canada affinity partner

If you’re curious about the rising cost of insurance premiums, you’re not alone. TD Insurance understands how the fast-moving insurance market has prompted many to question rate increases. This article explores the key drivers behind these changes and how they may affect you, offering guidance for Engineers Canada members and outlining steps TD Insurance is taking to provide competitive rates.

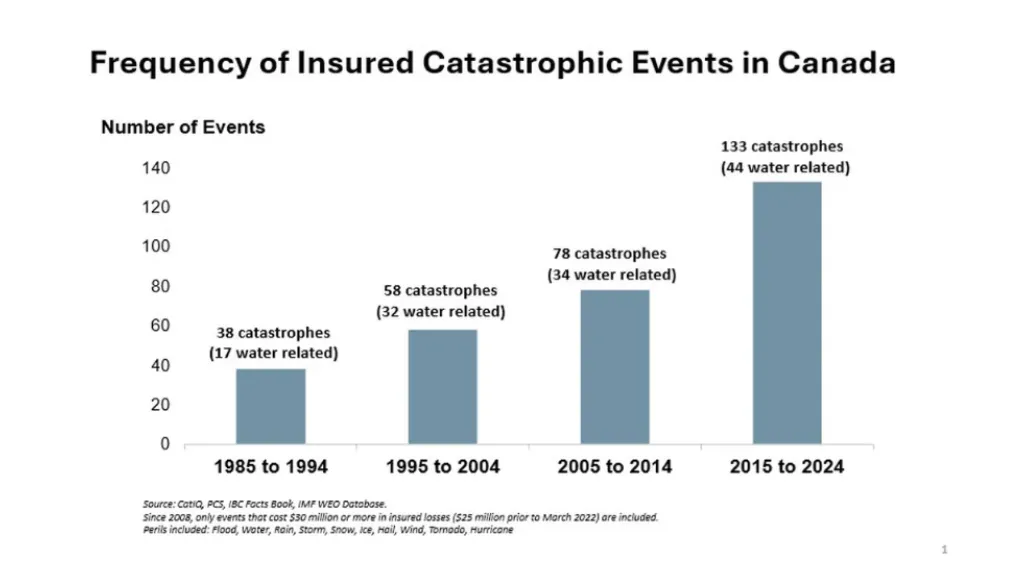

Impact of Severe Weather Events

In 2025, the Insurance Bureau of Canada reported $2.4 billion in severe weather-related insured damages, largely due to the March ice storm in Ontario & Quebec. Over the past twenty years, catastrophic weather-related losses exceeding $1 billion annually have become more frequent, putting pressure on the insurance industry and affecting premiums.

Figure 1 Frequency of Insured Catastrophic Losses in Canada. Sources: CatIQ, PCS, Insurance Bureau of Canada (IBC) Facts Book, International Monetary Fund World Economic Outlook Database

Inflation and Rising Costs

Inflation is driving up claims costs across the industry. The Statistics Canada Building Construction Price Index has recorded a 67 per cent rise in residential construction costs over five years, impacting the expense of repairs and replacements. These inflationary pressures challenge the property insurance market, leading to premium adjustments to maintain service quality.

Uncertainty of Tariffs

Geopolitical tensions, U.S. tariffs, the war in Iran, a weaker Canadian dollar, and supply chain disruptions have all contributed to rising costs for consumers and businesses. These factors especially affect the energy, automotive, and consumer goods sectors, leading to higher repair expenses and longer repair times, which further increase claims costs.

Auto Theft

Auto theft claims in Canada are now 371 per cent higher than a decade ago, according to Équité. While government and industry efforts have helped reduce theft, low recovery rates and higher replacement costs for newer vehicles continue to impact auto insurance premiums.

Auto Insurance Reforms in Ontario

Regulatory changes in Ontario, effective July 1, 2026, will make nine mandatory Accident Benefits sub-coverages optional. Insurers will be the first payors for medical and rehabilitation benefits in all auto accidents. These reforms aim to provide more flexibility and choice for consumers, enabling them to tailor coverage and premiums to their needs.

Auto Insurance Reforms in Alberta

The Insurance Bureau of Canada reports Alberta’s major auto insurance reforms will take effect January 1, 2027, following significant losses among insurers. These changes aim to stabilize the market and promote sustainability.

Industry Resilience and Adjustments

TD Insurance has adjusted its residential and auto pricing across Canada, considering claim frequency, severity, costs, and reinsurance pressures. The aim is to keep delivering excellent service and value with diverse products and pricing options.

Advice, Resources and Ways to Save

We invite you to explore these resources:

- The TDI Advice Centre provides insurance advice, articles, videos, and information on how home insurance premiums are calculated.

- TD Insurance offers over 30 Ways to Save on home and auto insurance, including member discounts, rewards for claims-free policies, incentives for hybrid/electric vehicles, and anti-theft devices.

- TD MyAdvantage delivers a personalized auto insurance experience, integrated into the TD Insurance Mobile app, with a one-time 10 per cent activation discount if enrolled within 10 days. Average discounts in Ontario exceed 11 per cent.

- The TD Insurance Fraud Hub helps Canadians understand and protect against insurance fraud.

As we look ahead to 2026, TD Insurance thanks you for your loyalty. With ongoing risks from severe weather, stay prepared by visiting the TD Insurance Advice Centre for safety tips for you and your loved ones.

As a trusted partner, the Engineers Canada-sponsored program with affinity partner TD Insurance is dedicated to helping engineers and geoscientists get access to preferred insurance rates. These preferred rates are available on car, home, condo and tenant coverage.